Rugby Spread Betting UK: Beyond Fixed Odds with Spreadex and Sporting Index

Loading...

How spread betting reframes the rugby punter’s mathematics

The first spread bet I ever placed was on the 2011 World Cup quarter-final between France and England. I sold the French supremacy spread at five points, expecting a tighter contest than the book implied. France won by seven. The match was over for me as a spectator at the eightieth minute, but the bet was over much earlier — the supremacy made up at twelve points, my position lost seven times my stake, and I learned the single most important fact about spread betting in twelve minutes of actual play. You do not bet to be right. You bet to be right by a specific amount.

That distinction matters because spread betting on rugby is structurally different from everything else in the UK betting market. Your stake is not your maximum loss. Your stake is a multiplier on the gap between the make-up number and your entry point. A one-pound stake on a supremacy spread can produce a thirty-pound win if the favourite covers, or a thirty-pound loss if the result swings the other way. That asymmetry has consequences, and the consequences are not always in the punter’s favour. The rest of this article is what nine years of running rugby spread positions has taught me about when the structure helps, when it hurts, and how to use it intelligently.

How a spread quote works — make-up, buy, sell

The mechanics first, because nothing else makes sense without them.

A spread firm — Spreadex or Sporting Index in the UK rugby market — publishes a two-way quote on a rugby outcome. The quote takes the form of a range: for a Six Nations match, the supremacy spread on the favourite might be published as 5-7. The five is the “sell” price; the seven is the “buy” price. The gap between them is the firm’s margin, equivalent to the over-round on a fixed-odds book.

If you “buy” the supremacy at seven, you are betting that the favourite will win by more than seven points. For every point the favourite wins by above seven, you win one times your stake. For every point below seven (including the favourite losing), you lose one times your stake. If you “sell” at five, you are betting the favourite will win by less than five points. For every point below five — including draws and losses by the favourite — you win one times your stake. For every point above five, you lose one times your stake.

The “make-up” is the final number the result settles at. In our example, if the favourite wins by ten, the make-up is ten. A buyer at seven wins three times their stake. A seller at five loses five times their stake. If the favourite wins by exactly six, the make-up is six — buyer at seven loses one times stake, seller at five loses one times stake (yes, both lose; that is the firm’s edge, which is why the spread exists).

Spread quotes update continuously as the match progresses. A live supremacy spread will widen or narrow based on actual scoring, time remaining, and player availability. Cash-out exists on most spread positions, expressed as the current spread minus a small margin. You can close a position at any point in the match by trading the opposite direction at the prevailing live quote — buy if you originally sold, sell if you originally bought.

The total points spread works the same way but on combined match score. The performance spreads — which we will get to — use specific scoring tariffs that the firm publishes per market.

The single most important thing to absorb from this section is the multiplier effect. A two-pound stake on a supremacy spread is not a two-pound bet. If the result moves twenty points against your position, you owe forty pounds. The firm will close the position if your account balance falls below the maintenance margin, but that is small comfort if the swing is fast and large. Spread betting is leveraged, in the practical sense of the word, even when no formal margin is referenced.

Why spread firms sit under FCA, not the UKGC

This regulatory detail is worth a section because it shapes everything about how spread firms operate in the UK rugby market.

Fixed-odds bookmakers — the operators who publish a Six Nations 1X2 at fractional or decimal odds — are licensed and regulated by the UK Gambling Commission. The UKGC sets affordability rules, deposit-limit requirements, advertising standards and game-design constraints. The bet is treated as a wager under gambling law.

Spread firms operate under a different framework. Spreadex and Sporting Index are authorised and regulated by the Financial Conduct Authority because their products are classified as financial spread bets — derivatives whose value is tied to an event outcome. The FCA framework treats these positions as financial instruments, which means client funds are protected by the Financial Services Compensation Scheme up to a statutory limit, the firms must publish risk disclosures, and the conduct rules around client communications are more closely aligned with financial services than with the UKGC’s gambling-focused regime.

What this means in practice for the punter is fourfold. First, your money sits in client-segregated accounts under FCA rules, not in operator-pooled accounts under UKGC rules. The protection is structurally tighter. Second, the advertising and onboarding flow is more conservative — appropriateness assessments are required before you can open a spread account, and there is a more demanding sign-up process than the typical fixed-odds operator. Third, the firms must publish loss warnings and risk disclosures that you are required to read before placing a position. Fourth, the dispute resolution pathway goes through the FCA framework — including the Financial Ombudsman Service in serious cases — rather than through the UKGC-affiliated alternative dispute resolution providers.

The trade-off for the punter is that spread firms are slower to onboard and more demanding upfront, but the regulatory protection on your funds is more robust once you are inside the system. As Grainne Hurst, the BGC’s Chief Executive, put it earlier in 2025 when commenting on the broader UK betting landscape: “Raising taxes further now on regulated betting and gaming through a new single tax would be utterly self-defeating for the Government, while making a mockery of their growth strategy.” The point applies equally to spread firms — they are part of the regulated UK ecosystem that contributes to a sector worth roughly 17.2 billion pounds in revenue for the 2025-26 period, and the regulatory framework that protects punters depends on continued investment in that ecosystem.

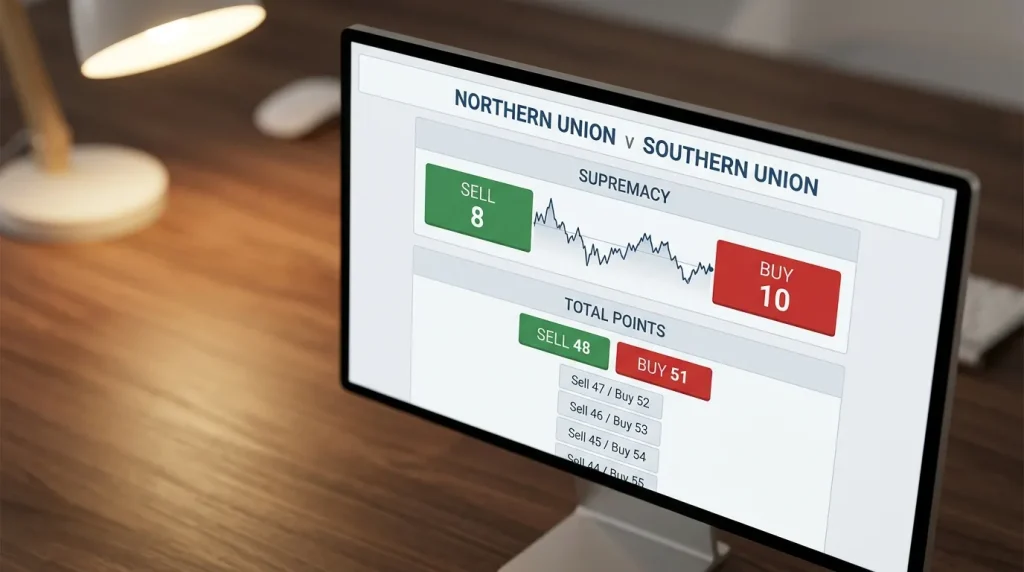

Supremacy and total points spreads on rugby

These two markets are the workhorses of rugby spread betting. Understanding both, and understanding how they relate to each other, is the foundation for everything that comes after.

The supremacy spread, as we have already touched on, is the predicted winning margin. The firm posts a range — say, 8-10 on a heavy Six Nations favourite — and the punter takes one side or the other. The supremacy spread is the closest analogue to the handicap line on a fixed-odds book, but the payout structure is fundamentally different. On the handicap, your stake is fixed and your payout is implied by the odds. On the spread, your stake is the per-point multiplier and your payout scales linearly with the result.

The total points spread is the combined match score range. A typical Six Nations total spread might be 48-51, meaning the firm expects the combined score to fall between forty-eight and fifty-one points. The buyer at fifty-one wins one times stake per point above fifty-one; the seller at forty-eight wins one times stake per point below forty-eight. Premiership totals tend to run higher because, as I discussed in the dedicated Premiership pricing piece, the league averaged 7.9 tries per match in the 2024-25 season. That higher try rate translates to total spreads typically published in the 50-55 band, sometimes higher when both sides are top-six clubs in attacking form.

The relationship between supremacy and total spreads is where structural value sometimes hides. Supremacy is a directional bet on the gap between two scores. Total is a directional bet on the sum of two scores. The two are mathematically independent in their straightforward form, but they are correlated in practice because a high-scoring match tends to produce higher absolute margins than a low-scoring match. If the firm prices supremacy and total such that the implied probability of a particular score pattern is internally inconsistent, you can construct a paired position that captures the inefficiency.

Worked example, using simple numbers. Suppose the supremacy spread is 10-12 and the total spread is 50-53. If the favourite wins 35-22, supremacy makes up at thirteen (buyer at twelve wins one times stake), total makes up at fifty-seven (buyer at fifty-three wins four times stake). If the favourite wins 28-15, supremacy makes up at thirteen (same), total makes up at forty-three (seller at fifty wins seven times stake). The combined paired position would be: buy supremacy at twelve, sell total at fifty. That captures the favourite winning by a substantial margin in a low-scoring match. If you have a directional view on a defensively dominant favourite, this paired position is more efficient than either single bet alone.

The catch, and it is a meaningful one, is that paired positions multiply your downside symmetrically. If you are wrong about the favourite, both positions lose. The losses can compound rapidly. Spread betting positions should be sized assuming both legs lose by the maximum plausible amount, not by the average.

One final pricing wrinkle. Wales and Italy fixtures consistently produce total spread results below the central line, and France at home consistently produces total spread results above. These structural patterns persist year after year because they reflect playing-style realities the spread firms cannot fully price out. Build them into your prior.

Performance and try-scorer spreads

This is where spread betting moves beyond the equivalents of fixed-odds markets and into territory that no fixed-odds book replicates. Performance spreads are bets on the cumulative point-tariff value of a player or team’s contributions to a match. Try-scorer spreads use specific scoring schedules — typically, twenty-five points for a first try, ten for any subsequent try, three for a conversion, two for a penalty — and the make-up is the sum across the player or team for the match.

A typical individual try-scorer spread on a tier-one winger in a Premiership match might be 18-22. A buyer at twenty-two needs the player to accumulate more than twenty-two performance points, which roughly translates to one try plus a try-related contribution, or two tries with no related contribution. A seller at eighteen needs the player to do less than that. The granularity is unique to spread betting — no fixed-odds book offers a market this responsive to nuanced individual contribution.

The supremacy performance spread is similar but team-level: cumulative team contributions valued by the firm’s scoring schedule. A team supremacy performance spread of 25-28 means the firm expects the favourite to outscore the underdog by twenty-five to twenty-eight contribution points across the match. Buyers and sellers operate as before.

The bookings-and-discipline spreads are a niche but interesting market. The make-up is the cumulative points awarded for sin-bins (typically ten points each) and red cards (twenty-five points each). On heavily-refereed matches — Six Nations openers, World Cup knockouts — the bookings spread is sometimes mispriced low, because the actual disciplinary intensity exceeds the firm’s pre-match expectation.

For tournament-long performance spreads, the firms publish make-ups on top try-scorer of a tournament, top points-scorer, total tries in a tournament, and other aggregates. These are essentially long-duration positions equivalent to ante-post bets, with the spread mechanics applied. The Six Nations sponsorship landscape — with Guinness alone running at fifteen million pounds per year across both Championships — gives you a sense of the commercial significance of the tournament, and the spread firms reflect that significance in the depth of markets they publish across the Championship. There is no other rugby tournament where performance spread markets are this deep.

The risk on performance spreads is that the multiplier can run further than on supremacy or total. A top winger having an exceptional match — first try, second try, third try, third conversion as cover kicker — can accumulate seventy or eighty performance points, against a typical pre-match spread of twenty. Buying at twenty-two and getting eighty in the make-up is a fifty-eight-times-stake win. The same dynamic in reverse, on a player who delivers nothing, is a small loss. The asymmetry — high upside on a hot performance, smaller downside on a flat one — is what makes performance spreads attractive when you have a strong view on a specific player.

Spreadex vs Sporting Index for UK rugby

The two major UK rugby spread firms operate slightly differently, and the differences matter when you are choosing where to open an account.

Spreadex is the broader of the two operators, with deep coverage across rugby union and rugby league alongside football, cricket and tennis. The rugby market depth is impressive — Spreadex publishes spreads on Six Nations from before the team announcements, follows Premiership and Top 14 fixtures with reliable lines, and runs tournament-long markets on every major event including the Lions tour and the Rugby World Cup. Their app is mature, the in-play feed is responsive, and the customer-service ladder is well-staffed. Where Spreadex genuinely shines is in coverage of niche tournaments — Currie Cup, Mitre 10 Cup, age-grade internationals — where the spreads are available even when liquidity is thin.

Sporting Index is the more rugby-focused historically, and the depth of their performance spreads on individual matches tends to exceed Spreadex in the most heavily-traded fixtures. Their try-scorer performance spreads on Six Nations matches typically offer the widest range of individually-priced players in the UK market — sometimes including replacement-bench wingers whose spread is available with reasonable liquidity. Their in-play modelling is excellent on the headline events, particularly Test matches where defensive structures are well-modelled. Their UI feels more spread-betting-native, which is a function of their longer corporate history in the space.

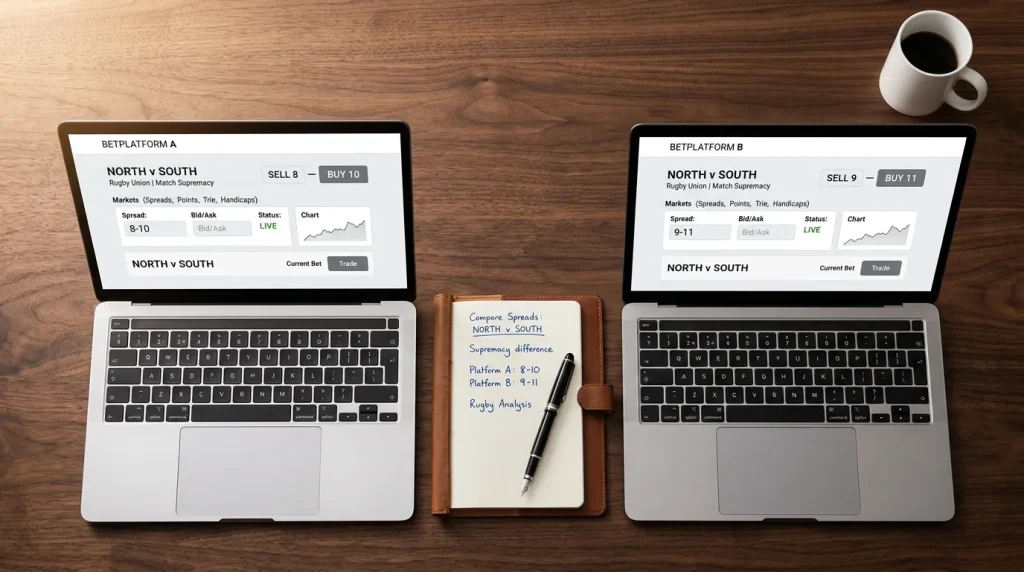

For a typical UK rugby punter, I would recommend opening accounts at both firms and comparing lines fixture by fixture. The cross-firm spread on a Six Nations supremacy is typically less than half a point, but on niche markets — particularly tournament-long performance spreads on individual players — the gap can be wider, and the more favourable price compounds across a tournament-long position.

One operator-specific feature worth noting is how each firm handles controlled risk positions. A controlled risk bet — one where your maximum loss is capped at a stated amount even if the result moves further — is available on most fixed-odds book equivalents but is structured differently on spread firms. Spreadex offers controlled risk on a wider range of rugby markets than Sporting Index. The cost of the controlled risk is built into the spread (the buy price is slightly wider, the sell price slightly narrower), and the trade-off is worth it for newer spread punters or for anyone whose bankroll cannot absorb a worst-case scenario.

For deeper context on how the fixed-odds handicap relates to the supremacy spread, including specific worked examples of when each is the more efficient way to take a directional view, I keep referring back to my walk-through of the rugby handicap line, which forms the foundation for understanding spread mechanics by extension.

Risk management — closing out, stop-losses, controlled risk

This is the section that should keep you out of trouble. Spread betting risk management is not optional; it is the difference between a profitable year and a catastrophic one.

The first principle is stake sizing. The per-point multiplier should be calibrated to a worst-case scenario you are willing to accept, not to your expected case. A common error is to size based on expected outcome — “I think the favourite will win by twelve, the spread is at ten, so the upside is two times my stake” — when the worst-case is the favourite losing by twenty, which would cost thirty times your stake. Always size to the downside. A reasonable rule for new spread punters is that the maximum loss on any single position should not exceed two per cent of your total bankroll.

The second principle is closing out. You can take any spread position off the table by trading the opposite side at the prevailing live quote. If you bought supremacy at twelve and the match is at half-time with the favourite up by fifteen, you can sell at, say, sixteen-eighteen — locking in a four-point profit on your buy price minus the spread firm’s margin. Closing out partially — selling half your buy position at sixteen — gives you the same protection on half your stake while leaving you with full upside on the remaining half. Partial closing is the spread bettor’s most useful tool, and it should be a habit, not an exception.

The third principle is the stop-loss. A stop-loss is an automatic close-out triggered when the spread moves to a stated level against your position. If you buy supremacy at twelve, you can set a stop-loss at five — automatically closing your position if the live supremacy falls to five. Stop-losses prevent the worst-case scenarios from spiralling. The trade-off is that stop-losses sometimes trigger during temporary swings (a yellow card to the favourite causes the supremacy to drop sharply before recovering), and you can be stopped out of a position that would have recovered. Use stop-losses at levels that reflect your tolerance for noise, not at levels that capture every wiggle in the live quote.

The fourth principle is the controlled risk product. A controlled risk position has a built-in maximum loss — typically published as part of the position’s terms — that cannot be exceeded regardless of how the make-up resolves. The cost is a wider spread, which means lower upside, but the trade-off is structural protection. For new spread punters, controlled risk should be the default, not the exception. As you build experience and confidence, you can reduce reliance on controlled risk in favour of stop-losses, which are cheaper but require active management.

The fifth principle is the broader UK context. The 2025 H2 Gambling Capital research put the offshore black market for UK betting at roughly 16.6 billion pounds — triple the 2019 figure — which underlines why the regulated FCA-supervised spread firms are the only sensible home for rugby spread punters. The offshore alternatives offer no protection on funds, no dispute resolution, no risk disclosure standards. The cost of using a regulated firm — slightly wider spreads, FCA-required risk warnings, slower onboarding — is a small price for the structural safety it buys you.

When a spread is sharper than a fixed-odds market

The honest answer is that spread betting is not always the right product. For most rugby punters most of the time, the fixed-odds handicap and totals markets are simpler, more transparent, and more forgiving. Spread betting earns its place in three specific scenarios.

First, when you have a strong directional view on the magnitude of a result, not just the direction. If you think the favourite will win comfortably — by, say, fifteen-plus points — the fixed-odds handicap caps your upside at the implied probability of covering the line. The spread, by buying supremacy aggressively, gives you upside that scales linearly with the magnitude of your correctness. Twenty-point wins by the favourite pay much more on the spread than on the fixed-odds handicap.

Second, when the market you want does not exist on the fixed-odds book. Individual performance spreads, team-level performance spreads, time-windowed totals, exotic specials — these markets are spread-betting-native and rarely have meaningful fixed-odds equivalents. If you want to express a view on a specific winger’s total contribution to a Six Nations match, the spread is the only place where that view can be properly priced.

Third, when you want to construct paired positions that combine directional views across multiple markets in a single coherent bet. The example I worked earlier — buy supremacy, sell total — is a paired position that captures a specific match-pattern view. Fixed-odds books can replicate this only crudely through bet builders, and the conditional pricing inside a bet builder is rarely as clean as the independent pricing of two spread positions.

The cases where spread betting is worse than fixed-odds are also worth stating. If your view is small-magnitude — you think the favourite wins narrowly — the spread is rarely a better product than the underdog plus the handicap. If your bankroll is small relative to the per-point multiplier you are comfortable with, the spread amplifies variance in ways that may not suit you. If you want to bet recreationally on the headline 1X2 outcome with no view on margin, fixed-odds is cleaner and the worst case is your stake.

Match your product to your view. Spread when your view is about magnitude or about something the fixed-odds book does not price. Fixed-odds when your view is binary and your bankroll demands clear maximum loss.

Where spread betting fits in a rugby punter’s toolkit

Spread betting on rugby in the UK is a specialised tool, not a default. It rewards punters with strong directional views on magnitude, with the discipline to size positions to worst-case downside, and with the patience to navigate FCA-regulated onboarding for the structural protections it provides. Used correctly, the spread firms give you access to markets that no fixed-odds bookmaker can match, and the leverage works in your favour when your view is right and well-sized. Used poorly, the multiplier effect can hollow out a bankroll in a single afternoon. Treat it as a precision instrument. Bring a directional view, size your stake to the downside, and respect the regulatory framework that exists to protect you. The spread, when it earns its place in your toolkit, is the sharpest single market in UK rugby betting.

Frequently asked questions about rugby spread betting

Is rugby spread betting riskier than fixed-odds betting?

Yes, structurally. On fixed-odds, your maximum loss is your stake. On spread, your loss scales with how far the result moves against your position, multiplied by your per-point stake. A small per-point stake can produce a large loss if the swing is big. Controlled risk products cap this loss at a stated amount, but at the cost of a wider spread. New spread punters should default to controlled risk positions until they understand the magnitude of swings they are willing to absorb.

How is a make-up calculated on a Six Nations supremacy spread?

The make-up is the actual point difference at the final whistle. If France beat Wales 28-10, the supremacy make-up is eighteen — France ahead by eighteen points. If you bought supremacy at twelve, you win six times your stake. If you sold at ten, you lose eight times your stake. The make-up settles at the full-time score, after any final-play conversions, and is not affected by extra time unless extra time is part of the contest format (which is unusual for Six Nations matches but applies in some knockout tournaments).

Can losses on a spread bet exceed the original stake?

Yes, on standard spread positions. The per-point multiplier means your stake is the amount you win or lose per point of movement, not the maximum you can lose. A two-pound stake on a supremacy spread can produce a loss many times that two pounds if the result moves substantially against you. Controlled risk positions are an exception — they cap the maximum loss at a stated amount that cannot be exceeded — but standard spreads carry no such cap.

Which UK firm holds the deepest tournament spread range on rugby?

Both Spreadex and Sporting Index publish deep tournament-long markets on the major rugby events, with most coverage during Six Nations, the Lions tour and Rugby World Cup cycles. The performance spread depth — individual player markets, tournament-long try-scorer markets, exact-margin spreads — tends to be marginally deeper at Sporting Index for Test rugby, while Spreadex offers broader cross-tournament coverage including niche fixtures. Opening accounts at both firms and comparing fixture-by-fixture is the standard approach for serious UK rugby spread punters.

Recommend

Written by the editors at Rugby Betting Sites.